Understanding “When Does Gap Insurance Not Pay” is crucial for any vehicle owner relying on this coverage. This comprehensive guide explores the various scenarios and exclusions where gap insurance won’t provide coverage, including missed payments, repossession and vehicle depreciation. Learn about the limitations and common reasons for denied claims to ensure you are fully informed and prepared.

🚗💥 Gap Insurance Coverage Details 💥🚗

Whenever the economy suffers setbacks, whatever is missing, your gap insurance takes care of it! It comes in handy for those elongated instances when a vehicle gets diagnosed as a total loss, whether from a nasty accident or due to theft. No longer, he said with kind of a mirthful exasperation, paying the difference between the worth of the car and the amount one has remaining on the loan for the said car – that is what gap insurance aims to achieve.

Thanks to the gap between the amount you will get for your insurance policy and the amount you owe your lender, you will never worry about this. Car owners will appreciate the fact that it also covers the loss against total loss due to floods as well as loss from the very unpredictable occurrence of theft.

What is Gap Insurance and Why Is It Important?

As it’s known as GAP or Guaranteed Asset Protection insurance, it refers to the additional vehicle insurance coverage that comes in handy for any borrowers mainly in vehicle leases or vehicle finance. Especially new cars experience quick depreciation and in their first few years, it would be possible for the market value to be less than the amount of loan on the vehicle.

Take for example, if car meets an accident and is badly in wreckage and cannot be saved or it is stolen, the first party auto insurance coverage would only pay what the damaged vehicle is worth, known as the actual cash value, which leaves you still owing money on your loan. That’s where Gap insurance comes into play; it helps pay for the gap so that you don’t have to reach into your pocket when you can no longer use your car.

Nevertheless, there are still limitations to the application of such insurance which some drivers overlook. Studying the exclusions and limitations of your gap insurance coverage can better equip you and avoid unpleasant surprises.

Key Situations Where Gap Insurance Won’t Pay

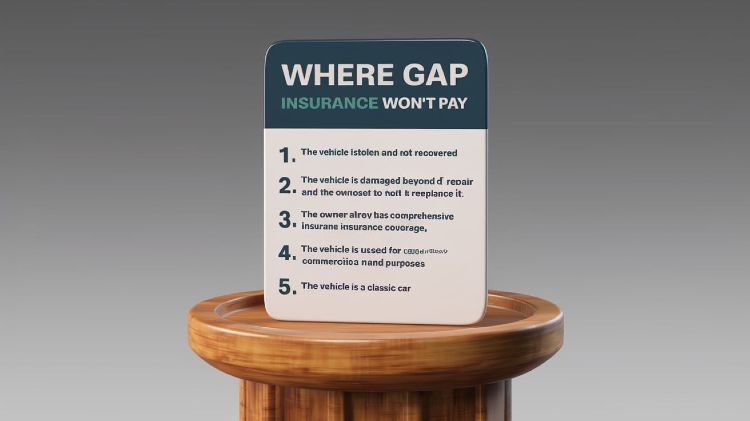

1. Missed or Late Loan Payments

One of the primary situations why gap insurance will not pay out is if there are unpaid repayments or repayments are made after the due date,” missed or late payments on your loan. Gap insurance does not provide reimbursement for any fines, costs or fees charged because a payment was made late. This includes any penalty that applies to the borrower due to late or missed repayments on the loan.

2. Non-Total Loss Accidents

This insurance had only one purpose in its creation and that was to make up for the cases of total loss. However, if the vehicle is damaged but not a total loss in the eyes of the primary insurer, gap cover will not apply. For example, in case the repair cost incurred is less than the market value of the vehicle say a small margin, make the insurer at risk not total loss and gap cover will not apply.

3. Gap Insurance Exclusions: Add-Ons and Extras

In addition to the car loan, there are some other costs that every borrower pays such as extended warranties, service contracts or coverage such as the gap itself, paint protection or aftermarket parts. These items are accrued to the loan but such items are beyond the reach of the gap insurance coverage. If you financed these extras hence bruise your loan balance, rest assured you will not be paid up for these.

4. Gap Insurance Not Paying Off Loan Due to Depreciation

Wear and Tear is key not only to one’s car but to the very limits that gap insurance covers. The extent of the gap insurance will only cover the remaining sums that exist between the worth of the vehicle as at the time and the owed sums not the depreciation as a result of use. In scenarios where the rate of depreciation of the car surpasses the insureness, there are chances that a person will be at a loss with regards to the insurable coverage.

5. Situations Where Gap Insurance Won’t Pay Due to Repossession

If your car is taken away by the lender because you do not repay the loan, you will not get the rest of the loan amount from gap insurance that will remain after the repossession. For many people, there is a misconception regarding the gap insurance where people think that such insurance covers a car that has been repossessed. Quite the opposite, it only institute cases where the car is a total loss or parts thereof, has been stolen.

6. Negative Equity from Previous Loans

It is pretty standard to shift negative equity from a previous vehicle loan and add it into the current loan, but this is where gap insurance does not usually apply. Negative equity refers to the amount that the borrower is still owing on their previous shopping loan compared to how much the car that they wish to get is worth. Only the specific vehicle that the loan is taken against is insured.

7. Intentional Damage, Fraud, or Illegal Activities

Gapping insurance, for example, will not pay out for your claim in circumstances where you purposefully damage your vehicle, or commit fraud by pretending that the vehicle has been stolen or there is a staging of car accidents. In the same way gap insurance is not active when the loss or accident is done by the imbiber of drugs and alcohol or any other crime, then it’s not active.

Additional Resources and Further Reading on Gap Insurance

Insurance Information Institute (III): The III is a reputable source for insurance-related information and provides comprehensive details on various insurance types, including gap insurance.

Link: Insurance Information Institute

National Association of Insurance Commissioners (NAIC): The NAIC offers information on various insurance products, including gap insurance.

Link: NAIC

Why Gap Insurance Didn’t Pay: Common Reasons for Denied Claims

There are reasons why you may need an explanation on the refusal or denial of gap insurance coverage, reasons that make you look for harmful demise depending on the claim you have made. Here are the most common reasons:

- Failure to Meet Total Loss Criteria: Gap insurance provides benefits only where the primary insurer regards the vehicle as a total loss. Should your primary insurer decide not to classify the vehicle as a total loss, then there will be no gap insurance.

- Not Using Primary Insurance First: Gap insurance acts as a backup insurance policy such that it is only applicable after an auto insurance policy has settled. Any application for claim settlement on this policy will be rejected if there is no claim report done first on the first insurance company.

- Unpaid Balances on the Loan: Any unpaid balance on your loan such as … late fees… accrued interests… missed payments… will not be covered by Gap insurance. It is only a complement of the car during a loss. It covers the gap between the Acv of the car or the value upon resolution of the loan remaining balance at the time of loss.

- Coverage Limits Exceeded: This sometimes occurs when the gap insurance coverage amounts are more than the limit period stipulated. There is usually an index in forms of CPM’s in life insurance coverage that imposes a limit on further, any gap insurance remaining loan balance exceeding which will not be covered by gap insurance.

- Not Adhering to Policy Terms: In most cases of gap insurance, there are standard policy terms and some conditions that have to be fulfilled. Failure to meet these requirements such as lack of comprehensive coverage may give rise to a claim denial.

Gap Insurance Limitations: What You Need to Know

As though it were a wholly beneficial product, gap insurance comes with a few restrictions every policyholder ought to be aware of;

Coverage Period Limitations

The majority of gap insurance policies will cover the most demanding and riskiest portion of the car loan for the first few years, generally not more than, three to five years. If your loan period exceeds this timeframe then you become on your own as the loan gets riskier.

Financing Restrictions

Some of these gap insurance policies are effective only within ranges of the loan amount and continous periods of the interest rates. For instance, very high-interest rates or long durations may have no coverage for the gap insurance policy.

Maximum Payout Limits

There are gap insurance policies in which there are set limits above which the policy will not cover any further compensation. For example if the gap insurance policy is $50, 000 but the loan balance is $55, 000, the insured will be liable for the extra $5, 000.

No Coverage for Non-Original Owners

Gap insurance is mostly confined to the first owner of a car, truck or perhaps an SUV. When somebody gets a second hand vehicle that used to have a gap insurance, that particular insurance does not go with the car.

Does Gap Insurance Cover Repossession?

Does gap insurance cover repossession or taking back of a property? This is a common question with a simple answer: no. In the case where a car is taken back by the lender because the owner has not been able to meet his/her part of the financial obligation, the gap policy will not be able to take care of the amount of the loan that was left. Gap insurance applies where a car has been totaled through accidents, theft, or any other covered event and total loss has occurred.

What Does Gap Insurance Cover?

There are certainly limits, and exclusions in the policy issued to individuals. However, knowing what gap insurance is not covers, is very crucial as well:

- Total Loss Due to Accidents: In the event that your car is in an accident and is paid a total loss, gap insurance will pay on the differential of what your vehicle is worth and the amount that you have left owing on the vehicle.

- Theft of the Vehicle: In the event where your or someone else’s cicada is stolen and goes unreturned, gap insurance pays out what is in excess of your insurer’s payout and the debt outstanding on the car.

- Natural Disasters: Despite the existence of such events, each applicant may be covered by gap insurance against total losses from natural disasters such as flood, hurricane, or fires, if comprehensive insurance is in place as well.

- Non-Financed Parts Not Covered: Finance gap protection is provided to cover the financed cost of the car itself and no non-financed cost and items within the scope of the car are covered.

[wptb id=771]

FAQs About Gap Insurance

Q1: Can I buy gap insurance after purchasing my car?

Yes, many insurers and dealerships offer gap insurance after the car purchase, but the cost and terms may vary. It is best to purchase gap insurance as soon as possible to avoid coverage gaps.

Q2: Will gap insurance pay if I still owe money on a car that was repossessed?

No, gap insurance does not cover loans for vehicles that are repossessed. It is only valid for total losses due to theft or accidents.

Q3: Does gap insurance cover damages from natural disasters?

Yes, there is a provision for gap coverage in case comprehensive insurances cover the loss, that is where your car is assessed as a total loss.

Q4: Can gap insurance cover rental car expenses?

No, gap insurance does not cover rental car expenses or any costs associated with replacing your vehicle. It only covers the difference between the car’s market value and the remaining loan balance.

Q5: Is gap insurance mandatory for leased vehicles?

There do exist cases when a gap insurance is not compulsory by law, but still some leasing companies offer it due to economics reasons.

Conclusion

A gap insurance is an excellent safeguard to avoid losses due to theft or total loss of a vehicle, but it is equally important to appreciate what it will not cover. Additionally, understanding the circumstances under which gap insurance does not apply (for example, your vehicle is repossessed, you stop paying and other such events) can assist you in planning accordingly so that such situations do not arise. It goes without saying that if you have an insurance cover, you should check the conditions of the cover in advance and check with your insurance company what is chewed by the coverage and what is not.

Gap insurance cannot be a cover in all cases; therefore, it is advisable to be aware of the situations under which a gap insurance may not be relied on.